Content

The distinction between capital assets and ordinary assets is usually the timeframe in which the asset is going to be a used. Inventory is bought and sold as part of the normal course of business, so it is an ordinary asset. Capital assets are usually classified as long-term assets on the balance sheet, whereas ordinary assets are usually classified as short-term. An ordinary asset is an item that holds future economic value to a company or individual, and that future economic benefit is expected to be used within the next year. For example, cash is an ordinary asset because it used to operate a business every day.

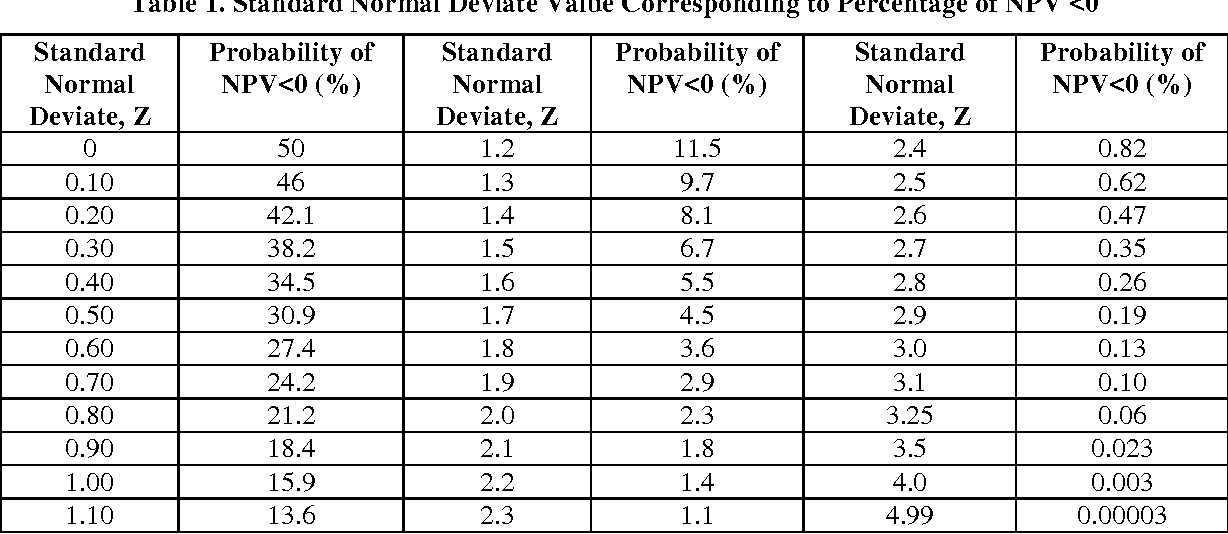

Empirical studies have demonstrated that unsystematic risk can be virtually eliminated in portfolios of 30 to 40 randomly selected stocks. Of course, if investments are made in closely related industries, more securities are required to eradicate unsystematic risk. There are no new reporting requirements and the update expands the current https://business-accounting.net/ prescription. The PDF is formatted to highlight the different categories of account codes and for printing. For display purposes, the account codes contain decimal points which should be excluded in your annual report. The basis of accounting selection will limit the BARS accounts that are applicable to the basis of accounting selected .

Tangible Assets

Addition of Quality or Quantity of Output - Additions that add to the quality or quantity of output should be depreciated over the remaining life of the original equipment. The original equipment must have a remaining life exceeding one year for this to apply. At the election of the taxpayer, paragraphs and of subsection shall not apply to musical compositions or copyrights in musical works sold or exchanged by a taxpayer described in subsection . Which is based on any current, objectively determinable financial or economic information with respect to commodities which is not within the control of any of the parties to the contract or instrument and is not unique to any of the parties' circumstances. For a list of Comptroller-controlled assets, see SPA’s Controlled Property Class Codes.

Amplifying this systematic variability in revenues is high operating and financial leverage. The results are earnings and returns that vary widely and produce high betas in these stocks. Major chemical companies exhibit an intermediate degree of systematic risk.

Capital Assets vs. Ordinary Asset

In most cases, businesses can deduct expenses incurred during a tax year from their revenue collected during the same tax year, and report the difference as their business income. However, most capital expenses cannot be claimed in the year of purchase, but instead must be capitalized as an asset and written off to expense incrementally over a number of years. The phrase "capital assets" isn't used on financial statements; instead the balance sheet will be broken into current assets and long-term assets. With its insight into the financial markets’ pricing of securities and the determination of expected returns, CAPM has clear applications in investment management.

Additional details about object codes are available in the BARS Manual 1.4. A company can choose the rate to depreciate its capital assets What Is a Capital Asset? however scenarios like this may result in a capital asset’s book value differing from the present market value of those very assets.

Capital Asset Management

In theory, the company must earn this cost on the equity-financed portion of its investments or its stock price will fall. If the company does not expect to earn at least the cost of equity, it should return the funds to the shareholders, who can earn this expected return on other securities at the same risk level in the financial marketplace.

- The lease liability should be measured at the present value of payments expected to be made during the lease term .

- The well-diversified CAPM investor would view the stock as a low-risk security.

- The cash basis financial reporting requirements for capital assets are limited; however, this does not remove the responsibility of the government from its stewardship of public resources.

- The most commonly used of these is a simple discounted cash flow technique, which is known as the dividend growth model (or the Gordon-Shapiro model).

- However, if the item is one that is diminished by display or educational or research applications, then the item should be depreciated over its estimated useful life.

- All books, publications, and audio visual material purchased and owned by the Library with a useful life of more than one year will be capitalized without regard to purchase price.

It helps companies generate and maximize revenue and obtain long-term financial benefits, especially in a business environment. Where the sale of a capital asset results in a loss, the amount of loss that may be deducted is subject to limitations. Generally for individuals, capital losses may be used to offset capital gains and up to $3,000 of ordinary income. In addition, unused capital losses for a tax year may be carried over by individuals to future years. For State or Local governmental accounting in the United States with reference to public capital or infrastructure a capital asset is defined as any asset used in operations with an initial useful life extending beyond one reporting period. Generally, government managers have a "stewardship" duty to maintain capital assets under their control.

Property which a business intends to use to generate revenue and expects its usefulness to exceed one year. On a balance sheet, capital assets are represented as property, plant, and equipment (PP&E). Businesses may depreciate capital assets over the course of their expected useful life.

Is a laptop a capital asset?

Capital assets are also sometimes referred to as fixed assets. They can be equipment, machinery, computers, cars or anything that has quite a high cost and is going to be useful for your business for more than about a year.

When this adjustment is recorded, it will be recognized as a loss on the company’s income statement. An example to illustrate this is when a company may put its property on sale for the purpose of purchasing a larger property located in a busier or more ideal district. He owns the grocery store buildings; he lets out a small portion of some of the building to another party and receives rental income.

BARS Alerts

Encumbrances – Commitments related to unperformed contracts for goods or services should be utilized to the extent necessary to assure effective budgetary control and to facilitate cash planning. Encumbrances outstanding at year end represent the estimated amount of expenditures ultimately to result if unperformed contracts in process are completed; they do not constitute expenditures or liabilities.

A lessor should recognize interest revenue on the lease receivable and an inflow of resources from the deferred inflows of resources in a systematic and rational manner over the term of the lease. The notes to financial statements should include a description of leasing arrangements and the total amount of inflows of resources recognized from leases. A lessee should recognize a lease liability and a lease asset at the commencement of the lease term, unless the lease is a short-term lease or it transfers ownership of the underlying asset. The lease liability should be measured at the present value of payments expected to be made during the lease term . The lease asset should be measured at the amount of the initial measurement of the lease liability, plus any payments made to the lessor at or before the commencement of the lease term and certain direct costs. Leases with initial total annual fixed lease payments of $20,000 or more, or total recurring future minimum lease payments of $100,000 or more, should be capitalized.